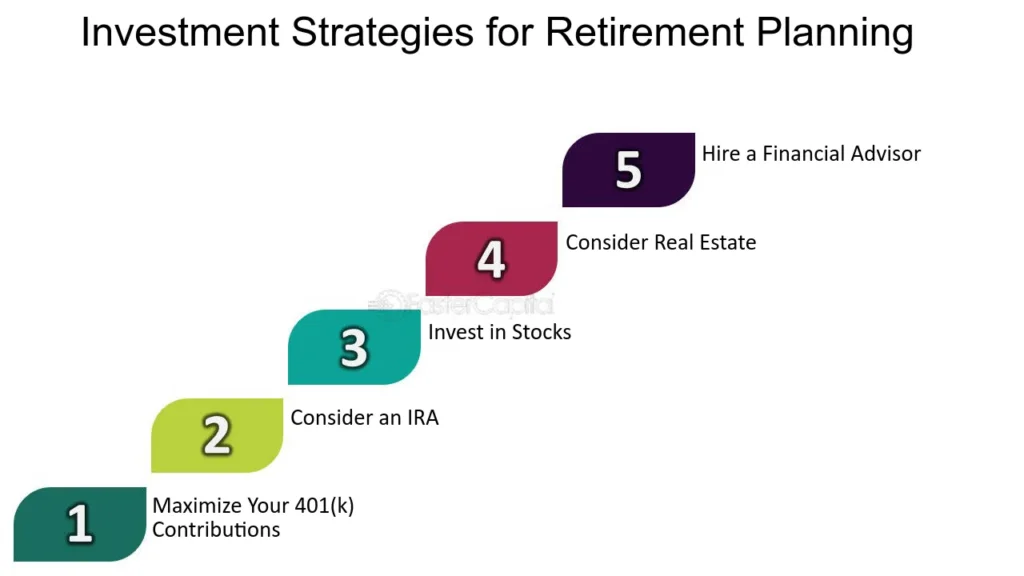

An effective strategy for retirement planning involves determining time horizons, estimating expenses, calculating required after-tax returns, assessing risk tolerance, and doing estate planning. It is important to start planning for retirement as soon as possible to take advantage of the power of compounding.

When it comes to investment allocation for retirement, it is best to have a diversified portfolio that includes a mix of stocks, bonds, and other assets based on your risk tolerance and investment goals. By structuring your retirement portfolio appropriately and considering factors such as expected returns and income sources, you can create a plan that helps you achieve your retirement goals.

Laying The Groundwork For Retirement

When it comes to retirement planning, laying the groundwork is crucial for a secure and comfortable future. This involves defining your retirement goals, estimating retirement expenses, and making strategic investment decisions. By taking these steps, you can ensure that you are on the right track to achieve financial stability in your golden years.

Defining Your Retirement Goals

Before you embark on your retirement journey, it is important to clearly define your goals. Ask yourself what you envision for your retirement years. Do you want to travel the world, spend more time with family, or pursue your hobbies? Understanding your goals will help you determine the amount of money you need to save and invest.

Estimating Retirement Expenses

Estimating your retirement expenses is a critical step in planning for your future. Start by considering your current lifestyle and how it may change in retirement. Factor in expenses such as housing, healthcare, transportation, and leisure activities. It is also important to account for inflation and any unforeseen circumstances that may arise.

One effective way to estimate your retirement expenses is to create a budget. This will give you a clear picture of your income sources and how much you can allocate towards different categories. By understanding your expenses, you can make informed decisions about your investment strategy.

Strategic Investment Decisions

Once you have defined your retirement goals and estimated your expenses, it is time to make strategic investment decisions. Your investment strategy should be tailored to your risk tolerance, time horizon, and financial goals. Diversification is key, as it helps to spread risk and maximize potential returns.

Consider consulting with a financial advisor who specializes in retirement planning. They can help you develop an investment portfolio that aligns with your goals and risk tolerance. Whether it’s investing in stocks, bonds, mutual funds, or real estate, a well-diversified portfolio can provide the growth and income you need for a comfortable retirement.

In conclusion, laying the groundwork for retirement involves defining your goals, estimating expenses, and making strategic investment decisions. By taking these steps, you can set yourself up for a secure and fulfilling retirement. Remember, it’s never too early to start planning for your future. The earlier you start, the more time you have to grow your wealth and ensure a financially stable retirement.

Early Planning Benefits

When it comes to retirement planning, early planning benefits cannot be overstated. By starting your retirement planning early, you can harness the power of compounding and set a savings timeline that allows you to build a substantial retirement fund.

Harnessing The Power Of Compounding

Compounding is the process where your investment earns returns, and those returns are reinvested to generate even more returns. Starting early allows your investments to grow exponentially over time, thanks to the power of compounding. This means that the earlier you start saving for retirement, the more time your money has to grow, and the larger your retirement fund can become.

Setting A Savings Timeline

Setting a clear savings timeline is essential for effective retirement planning. By determining how much you need to save and when you need to reach your retirement goal, you can create a structured savings plan. This timeline helps you stay on track and ensures that you are consistently contributing to your retirement fund, maximizing the benefits of compounding along the way.

Risk Tolerance Assessment

Assessing your risk tolerance is crucial for crafting effective investment strategies for retirement planning. By understanding how much risk you’re comfortable with, you can build a portfolio that aligns with your financial goals and comfort level, ultimately setting you up for a more secure retirement.

Before diving into investment strategies for retirement planning, it’s crucial to assess your risk tolerance. This assessment helps determine how much risk you are comfortable with when it comes to your investment portfolio. Factors such as age, financial situation, and future goals play a significant role in determining your risk tolerance.

Balancing Risk And Reward

When planning for retirement, it’s essential to strike a balance between risk and reward. Diversification across various asset classes can help manage risk while aiming for potential growth. Understanding your risk tolerance can guide you in finding the right balance between conservative and aggressive investments.

Adapting Strategy With Age

As individuals age, their risk tolerance often changes. Younger individuals may have a higher risk tolerance as they have more time to recover from market downturns. On the other hand, older individuals may opt for a more conservative approach to preserve their wealth. It’s important to adapt investment strategies in alignment with your age and evolving risk tolerance.

:max_bytes(150000):strip_icc()/retirement-planning.asp-FINAL-ed21279a08874c54a3a0f4858866e0b6.png)

Credit: www.investopedia.com

Investment Allocation Strategies

Retirement planning requires an effective investment allocation strategy that includes determining time horizons, estimating expenses, calculating required returns, assessing risk tolerance, and doing estate planning. It is important to start planning early to maximize the power of compounding and achieve financial goals in retirement.

Diversifying Your Portfolio

Diversification is one of the most important investment allocation strategies for retirement planning. It involves spreading your investments across different asset classes, such as stocks, bonds, and real estate, to minimize risk and maximize returns. By diversifying your portfolio, you can reduce the impact of market volatility and protect your savings from sudden downturns.

Considering Asset Classes For Retirement

When considering asset classes for retirement, it’s important to think about your investment goals and risk tolerance. Stocks offer higher returns but also come with greater risk, while bonds provide more stability but lower returns. Real estate can be a good option for long-term growth and income, but requires more upfront capital. It’s important to choose asset classes that align with your retirement goals and financial situation.

Optimizing Your Investment Mix

To optimize your investment mix, you should consider factors such as your time horizon, income needs, and tax situation. For example, if you have a long time horizon and can tolerate more risk, you may want to allocate more of your portfolio to stocks. If you need income in retirement, you may want to allocate more to bonds or dividend-paying stocks. And if you have taxable and tax-advantaged accounts, you may want to allocate your investments differently to maximize tax efficiency.

Monitoring And Adjusting Your Portfolio

Finally, it’s important to regularly monitor and adjust your portfolio to ensure it remains aligned with your retirement goals. This may involve rebalancing your portfolio to maintain your desired asset allocation, or adjusting your investment mix as your financial situation changes. By staying vigilant and proactive, you can optimize your investment allocation strategies for retirement planning and achieve your financial goals.

Tax-efficient Investment Tactics

Discover tax-efficient investment tactics for retirement planning. By considering time horizons, estimating expenses, and assessing risk tolerance, you can optimize your investment allocation for retirement. It’s crucial to start planning early to benefit from the power of compounding and make the most of your retirement savings.

Tax-Efficient Investment Tactics are a crucial aspect of retirement planning. These tactics help individuals maximize their investment returns and minimize their tax liabilities. Two popular tax-efficient investment strategies are Roth Conversions and Tax Gain Harvesting.

Roth Conversions

A Roth conversion is the process of moving funds from a traditional IRA or 401(k) to a Roth IRA. This conversion allows individuals to pay taxes on the converted amount at their current tax rate, rather than paying taxes on the amount withdrawn during retirement. Roth conversions can be beneficial for individuals who expect to be in a higher tax bracket during retirement. Additionally, Roth IRAs have no required minimum distributions, making them an excellent option for individuals who want to leave their investments untouched for a longer period.

Tax Gain Harvesting

Tax Gain Harvesting is a tax-efficient investment strategy that involves selling securities that have appreciated in value and realizing capital gains. This strategy is particularly useful for individuals who have taxable investment accounts. Tax gain harvesting helps individuals offset capital gains with capital losses and reduces their overall tax liability. Moreover, this strategy allows individuals to rebalance their portfolio without incurring additional taxes.

In conclusion, Tax-Efficient Investment Tactics are essential for effective retirement planning. Roth Conversions and Tax Gain Harvesting are two popular strategies that individuals can use to maximize their investment returns and minimize their tax liabilities. By incorporating these tactics, individuals can secure a more comfortable retirement and achieve their long-term financial goals.

Credit: www.linkedin.com

Retirement Income Planning

Retirement income planning involves implementing investment strategies that will help secure a comfortable financial future. By carefully considering time horizons, estimating expenses, and assessing risk tolerance, individuals can create a retirement portfolio that maximizes returns and ensures a stable income during their golden years.

Start planning early to take advantage of compounding and achieve long-term financial success.

Retirement Income Planning

When it comes to retirement planning, one of the most important aspects to consider is how you will generate income in retirement. Retirement income planning involves determining income sources and utilizing withdrawal rules to ensure you have enough money to support your lifestyle throughout retirement. Let’s dive into these two key areas in more detail.

Determining Income Sources

The first step in retirement income planning is to determine where your income will come from in retirement. This typically includes a combination of Social Security benefits, pension income, and personal savings. It’s important to understand how much you can expect to receive from each of these sources and how they will be taxed.

| Income Source | Expected Amount | Taxation |

|---|---|---|

| Social Security | $1,500/month | Partially taxable |

| Pension | $2,000/month | Fully taxable |

| Personal Savings | $500,000 | Tax-deferred or taxable |

Utilizing Withdrawal Rules

Once you have determined your income sources, the next step is to utilize withdrawal rules to ensure you don’t run out of money in retirement. One popular withdrawal rule is the 4% rule, which suggests withdrawing 4% of your portfolio balance each year in retirement. However, this rule may not be appropriate for everyone and it’s important to work with a financial advisor to determine the best withdrawal strategy for your individual situation.

Withdrawal Strategies

- Systematic Withdrawals: This involves withdrawing a fixed amount of money each year from your retirement accounts.

- Bucket Strategy: This involves dividing your retirement savings into different buckets based on when you will need the money and withdrawing from each bucket as needed.

- Variable Withdrawals: This involves adjusting your withdrawals each year based on market performance and your portfolio balance.

Retirement income planning is a critical component of retirement planning overall. By determining your income sources and utilizing withdrawal rules, you can ensure that you have enough money to support your lifestyle throughout retirement.

Estate Planning Essentials

Planning for retirement is essential, and investment strategies play a crucial role in ensuring a financially secure future. By considering factors such as time horizons, expenses, risk tolerance, and estate planning, individuals can create an effective retirement plan that takes advantage of compounding and maximizes returns.

It is important to start planning early to reap the benefits of long-term investments.

Estate Planning Essentials

Estate planning is an essential component of retirement planning that many people overlook. It involves creating a plan for your assets and how they will be distributed after you pass away. This can help ensure that your loved ones are taken care of and that your legacy is preserved.

Securing Your Legacy

One important aspect of estate planning is securing your legacy. This involves creating a plan for how your assets will be distributed after you pass away. You may want to consider setting up a trust or creating a will to ensure that your assets are distributed according to your wishes.

Understanding Estate Taxes

Another important aspect of estate planning is understanding estate taxes. Estate taxes can be a significant burden on your heirs if you haven’t planned for them properly. It’s important to work with a financial advisor or attorney to develop a plan that minimizes your estate tax liability.

Here are some tips for minimizing your estate tax liability:

– Make gifts to your heirs during your lifetime

– Set up a trust to hold assets

– Utilize the annual gift tax exclusion

– Consider life insurance as a way to provide for your heirs

By taking these steps, you can help ensure that your heirs receive the maximum benefit from your estate.

In conclusion, estate planning is an essential component of retirement planning. By securing your legacy and understanding estate taxes, you can help ensure that your loved ones are taken care of and that your assets are distributed according to your wishes. Work with a financial advisor or attorney to develop a plan that meets your unique needs and goals.

Monitoring And Adjusting Investments

Monitoring and adjusting investments is a crucial aspect of retirement planning. Conducting regular reviews and responding to market changes are essential to ensure that your investment strategy remains aligned with your retirement goals.

Conducting Annual Reviews

Conducting annual reviews of your investment portfolio is imperative to track its performance and make any necessary adjustments. During these reviews, assess the performance of individual assets, review the overall asset allocation, and evaluate the impact of market fluctuations.

Responding To Market Changes

Market changes can significantly impact the value of your investments. It’s essential to stay informed about market trends and respond proactively to mitigate potential risks and capitalize on opportunities. Be prepared to adjust your investment allocations based on changing market conditions to optimize your retirement savings.

Credit: www.rentecdirect.com

Frequently Asked Questions

What Is An Effective Strategy For Retirement Planning?

An effective strategy for retirement planning includes determining time horizons, estimating expenses, calculating required after-tax returns, assessing risk tolerance, and doing estate planning. Start planning for retirement as soon as possible to take advantage of the power of compounding.

What Is The Best Investment Allocation For Retirement?

The best investment allocation for retirement includes determining time horizons, estimating expenses, calculating required after-tax returns, assessing risk tolerance, and doing estate planning. Start planning for retirement early to benefit from compounding. Consider a diversified portfolio that includes a mix of stocks, bonds, and other investments based on your risk tolerance and goals.

Seek professional advice to ensure the right allocation for your specific needs.

What Is The 4% Rule In Retirement Planning?

The 4% rule in retirement planning suggests withdrawing 4% annually from your retirement savings. This rule aims to make your savings last throughout retirement.

What Investment Return Should I Use For Retirement Planning?

When planning for retirement, it is important to consider various factors such as time horizons, expenses, required after-tax returns, risk tolerance, and estate planning. Starting early and taking advantage of compounding can be beneficial. Consider consulting with financial professionals and exploring investment allocation options to create an effective retirement strategy.

Conclusion

Effective retirement planning requires careful consideration of various factors such as time horizons, expenses, required returns, risk tolerance, and estate planning. It is important to start planning as early as possible to benefit from the power of compounding. When it comes to investment allocation, it is advisable to consult professionals and consider a diversified portfolio that aligns with your goals and risk appetite.

By following these strategies, you can ensure a secure and comfortable retirement.

Olga L. Weaver is a distinguished figure in both the realms of real estate and business, embodying a unique blend of expertise in these interconnected domains. With a comprehensive background in real estate development and a strategic understanding of business operations, Olga L. Weaver has positioned herself as a trusted advisor in the complex intersection of property and commerce. Her career is marked by successful ventures in real estate, coupled with a keen ability to integrate sound business principles into property investments. Whether navigating the intricacies of commercial transactions, optimizing property portfolios, or providing strategic insights into market trends, Olga L. Weaver’s expertise encompasses a wide spectrum of both real estate and business-related topics. As a dual expert in real estate and business, she stands as a guiding force, empowering individuals and organizations with the knowledge and strategies needed to thrive in these intertwined landscapes. Olga L. Weaver’s contributions continue to shape the dialogue around the synergy between real estate and business, making her a respected authority in both fields.