Imagine unlocking financial possibilities by leveraging what you already own. Yes, your property can be the key to accessing funds when you need them most.

Whether you’re looking to start a business, cover unexpected expenses, or make a significant investment, using your property as collateral to secure a loan could be your solution. But how does it work, and is it the right choice for you?

We’ll walk you through the process of obtaining a loan using your property as collateral. You’ll discover the benefits, potential risks, and essential steps needed to make informed decisions. By the end, you’ll have a clear understanding of how to harness your property’s value to achieve your financial goals without diving into complex jargon or overwhelming procedures. Are you ready to explore the financial potential of your property? Let’s dive in and see how you can take control of your financial future.

Understanding Collateral Loans

Securing a loan with property as collateral offers a viable solution for many. Your property’s value often determines loan approval and amount. This type of loan generally provides lower interest rates, using your property as a guarantee. Understanding the terms is crucial to avoid potential financial pitfalls.

Understanding collateral loans can be a game-changer if you’re considering using your property to secure a loan. These loans can provide a pathway to accessing funds by leveraging the value of your assets. Whether you’re looking to expand your business, renovate your home, or tackle unexpected expenses, knowing how collateral loans work can open doors to financial opportunities.

Definition And Basics

Collateral loans are a type of secured loan where you use an asset, like property, as a pledge to the lender. This means the lender has a security interest in your property until you repay the loan. If you default, the lender can take the property to recover the loan amount. These loans often come with lower interest rates compared to unsecured loans. The reason? Lenders have less risk since they can claim your asset if you don’t pay back. This makes them a viable option if you’re looking for more favorable terms.

Types Of Collateral

Different types of assets can serve as collateral, depending on the lender’s terms. Real estate is a common choice, including your home or a piece of land. Cars, jewelry, and even savings accounts can also be used. Each type of collateral comes with its own set of requirements and value assessments. For example, using your home might mean a longer approval process due to property appraisals. In contrast, using a car might be quicker but could result in a lower loan amount. Have you ever wondered if your valuable assets could work harder for you? By understanding the different types of collateral, you can decide which option aligns best with your financial goals. It’s all about weighing the potential benefits against the risks involved.

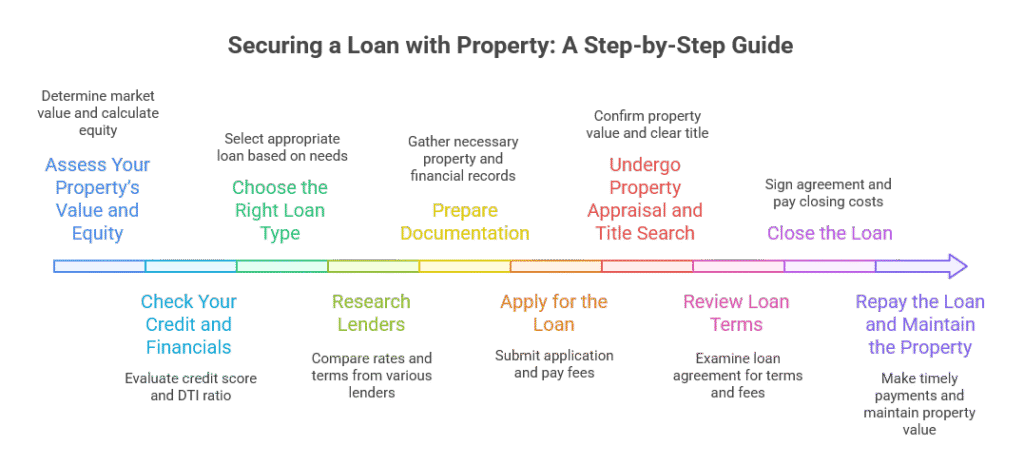

Steps to Get a Loan Using Property as Collateral

Hey there, looking to use your property to get a loan? It’s easier than you think. Follow these steps, and you’ll be on your way to securing those funds in no time.

Check Your Property’s Value

- Market Value: Get a professional appraisal to know your property’s worth. It might cost you $300–$700. You can also look at recent sales in your area for a ballpark figure.

- Equity Calculation: Subtract what you owe from your property’s value. For instance, if your home is worth $500,000 and you owe $200,000, you have $300,000 in equity.

- Borrowing Potential: Lenders usually let you borrow 70–90% of the property’s value. So, for a $500,000 home, you could get $350,000–$450,000.

- Tip: Online tools like Zillow can give you a quick estimate, but always go for a professional appraisal for accuracy.

Check Your Finances

- Credit Score: Aim for a score of 620–680. Higher scores, like 700+, can get you better rates. Check your score on websites like Experian.

- Debt-to-Income Ratio: Keep it below 43%. If you make $5,000 a month and pay $1,500 in debts, your ratio is 30%. Easy math, right?

- Tip: Improve your credit by paying off debts or fixing errors before applying.

Choose the Right Loan

There are different types of loans, each suitable for different needs:

- Home Equity Loan: It’s a fixed-rate loan for one-time expenses. Rates are around 8–10%.

- HELOC: A variable-rate credit line for ongoing expenses. Rates vary from 8.5–11%.

- Mortgage Refinance: Allows you to cash out and refinance your mortgage at 6.5–8% rates.

- Tip: Compare terms using APR, which includes all fees.

Find the Right Lender

Not all lenders are the same. Here’s what you need to know:

- Banks and Credit Unions: They offer good rates but have stricter requirements.

- Online Lenders: Quicker approval but higher rates.

- Private Lenders: More flexible for those with low credit but charge higher interest.

- Tip: Get quotes from at least three lenders. Compare the rates, fees, and terms.

Get Your Documents Ready

- Property Papers: Have your deed, title report, and mortgage statements ready.

- Appraisal Report: This confirms your property’s value.

- Financial Records: Two years of tax returns, recent pay stubs, bank statements, and proof of other income.

- Insurance Proof: Show that you have homeowners or property insurance.

Apply for the Loan

- Submit your application online or in person. Include all the paperwork mentioned above.

- Be prepared to pay application fees and appraisal costs.

- Tip: Be honest about your finances to avoid any delays.

Appraisal and Title Search

Two more steps to ensure everything’s in check:

- Appraisal: A licensed appraiser checks your property’s value.

- Title Search: Confirms that your property title is clear.

Review Loan Terms

Before signing anything, make sure you understand:

- Interest rates and repayment terms.

- Fees involved.

- Consequences of default.

- Tip: Consult an expert if things get too complex.

Close the Loan

- Sign the necessary documents.

- Pay closing costs.

- Get your funds, usually within a few days.

Repay and Maintain Your Property

- Make your payments on time. Default could lead to foreclosure.

- Keep your property in good shape to protect your investment.

That’s it! With these steps, you’re well on your way to securing a loan using your property as collateral. Good luck!

Assessing Your Property Value

Understanding property value is crucial for securing a loan using it as collateral. Banks assess property worth to determine loan eligibility. Accurate property valuation ensures appropriate loan amounts and repayment terms.

Understanding your property’s value is crucial for securing a loan. It determines the amount you can borrow. Knowing this value helps in negotiations with lenders. It also ensures you get the best deal possible. Let’s explore the key steps involved in assessing your property’s value.

Property Appraisal Process

The property appraisal process starts with hiring a professional appraiser. The appraiser evaluates the property’s condition and location. They compare it with similar properties recently sold. This comparison helps in determining a fair market value. The appraiser provides a detailed report of their findings. This report is essential for the loan application process.

Factors Influencing Value

Several factors influence your property’s value. Location is a significant factor. Properties in desirable areas often have higher values. The property’s size and condition also matter. Larger, well-maintained properties tend to be valued higher. Market trends can affect property values as well. Economic conditions and interest rates play a role too. Understanding these factors helps in making informed decisions. `

Choosing The Right Lender

Choosing the right lender when using your property as collateral is crucial to securing a loan that meets your needs. It can be overwhelming with numerous options available, but the key is to understand what each lender offers and how it aligns with your financial situation. It’s like shopping for a new car—you’re not just looking for the best deal, but also for reliability and support down the road.

Banks Vs. Private Lenders

When considering where to take your loan, you have two main options: banks and private lenders. Banks are often seen as the traditional choice, offering stability and a wide range of financial products. They might provide a sense of security, but can be rigid with criteria and slower in processing.

Private lenders, on the other hand, can be more flexible. They often operate with fewer restrictions, which might be beneficial if your credit score isn’t perfect. However, they might charge higher interest rates, so you’ll need to weigh the pros and cons. Think about what you value more: flexibility or lower costs?

Interest Rates And Terms

Interest rates and terms are the heartbeat of your loan agreement. Banks typically offer lower interest rates, but their terms might be less flexible. They might require a higher value of collateral or have longer approval times.

Private lenders might entice you with quicker approvals and less stringent requirements. However, be prepared for higher interest rates, which can increase your overall repayment amount. Consider what’s more important: saving on interest or getting quick access to funds?

Choosing the right lender isn’t just about numbers. It’s about the support they offer you throughout the loan process. Have you ever had to make a difficult financial decision? How did the support you received affect your outcome?

Remember, the lender you choose is your partner in this financial journey. Ensure they have your best interests at heart. It’s not just about securing a loan—it’s about making a wise choice that supports your financial goals. Are you ready to take this step confidently?

Preparing Required Documentation

Gather necessary documents to secure a loan using property as collateral. Include property titles, tax records, and income proof. Ensure all paperwork is accurate and complete to streamline the approval process.

Preparing the required documentation is a crucial step in obtaining a loan using your property as collateral. It can feel overwhelming, but with the right preparation, you can simplify the process. You’ll need to gather specific documents to prove your ownership and financial capability. Let’s dive into what you need and how to get it ready.

Proof Of Ownership

First, you’ll need to show that you actually own the property. This is where proof of ownership comes in. Your property deed is the most straightforward document to have on hand. A clear title demonstrates that you have no outstanding claims or disputes on the property. If you’ve ever purchased property, you know how important it is to keep this document safe. Have you ever misplaced a crucial paper? It’s frustrating! Make sure your deed is easily accessible and in good condition. If you can’t find it, request a copy from your local land registry office.

Financial Statements

Next, lenders will want a peek into your financial stability. This is where your financial statements come into play. Your recent bank statements, tax returns, and any income proof are essential. Are your finances in order? If not, now’s a good time to start organizing. Ensure you have statements for at least the last three months. This helps the lender assess your ability to repay the loan. You might think, “Is all this really necessary?” Yes, because these documents help build trust with your lender. They need to see a complete picture of your financial health. Preparing these documents might seem like a hassle, but it’s a critical step towards securing the loan. What else have you found useful when gathering important paperwork? Sharing your tips could help others streamline their documentation process.

Navigating The Application Process

Using property as collateral can simplify getting a loan. Yet, the application process might seem complex. Understanding each step can make things clearer and more manageable.

Filling Out Applications

Start with gathering necessary documents. These include property deeds, identification, and proof of income. Many lenders provide application forms online. Fill them out accurately. Mistakes can delay approval. Double-check all entries before submission. Include detailed information about the property. Highlight its value and condition. This information helps the lender assess risk.

Meeting Eligibility Criteria

Lenders have specific criteria for loan approval. Ensure your property meets these requirements. It should have a clear title. Any existing liens must be resolved. Your credit score is important too. A higher score increases approval chances. Prepare to demonstrate your repayment ability. Lenders may request proof of income or bank statements. Meeting these criteria improves your application’s success.

Understanding Loan Agreements

Getting a loan using property as collateral involves understanding loan agreements. These agreements detail the terms of your loan. Knowing what you’re signing is crucial. This knowledge helps prevent future surprises. Let’s explore key terms and the fine print.

Key Terms To Know

Loan agreements have specific terms. Interest rate is a major one. It shows how much you’ll pay for borrowing. Another term is the principal amount. This is the actual loan amount you receive. Loan term refers to the duration of your loan. Understanding these terms helps in decision-making.

Collateral is also a key term. It refers to the property used for the loan. If you default, the lender can seize this collateral. Default means failing to meet loan obligations. Grasping these terms prepares you for negotiations.

Reviewing Fine Print

Fine print contains important details. It may include hidden fees or penalties. Late payment penalties can add up quickly. Early repayment fees may also apply. These fees can impact your finances.

Fine print also details your responsibilities. It outlines what happens if you default. Understanding these details is vital. Seek clarification if something is unclear. A clear understanding prevents future disputes.

Managing Risks And Responsibilities

Obtaining a loan using property as collateral involves assessing risks and understanding responsibilities. Carefully evaluate property value and loan terms. Ensure repayment ability to avoid potential foreclosure.

Managing risks and responsibilities is crucial when using property as collateral. Using property for a loan can be beneficial. But, it involves significant risks. Understanding these risks helps in making informed decisions. Proper management ensures you fulfill your obligations. This keeps your property safe.

Potential Consequences

Failing to repay a loan can result in property loss. The lender may take ownership of the property. This is known as foreclosure. It can damage your credit score too. A poor credit score affects future loans. Consider the impact on your financial stability.

Safeguarding Against Default

Make sure to plan your repayments. Create a budget that includes loan payments. Set aside funds for emergencies. This helps avoid missing payments. Communicate with your lender if issues arise. They might offer solutions. Consider insurance for additional protection. This can cover payments in difficult times. Always understand the loan terms clearly. Ask questions if needed. Knowledge is your best tool against risks.

Leveraging Expert Advice

Leveraging expert advice can simplify the loan process. It provides guidance and boosts confidence. Experts help you understand complex terms and conditions. They ensure you make informed decisions. Their insights can prevent costly mistakes. This section explores consulting financial advisors and using online resources.

Consulting Financial Advisors

Financial advisors offer valuable insights into using property as collateral. They assess your financial situation thoroughly. Advisors guide you on loan terms and interest rates. They help identify the right loan type for your needs. Their expertise aids in understanding the potential risks involved. They also assist in preparing the necessary documents. This preparation makes the loan application smoother. Meeting with a trusted advisor can be a wise step.

Utilizing Online Resources

Online resources provide a wealth of information on loans. They offer detailed guides on using property as collateral. Websites often have calculators to estimate loan amounts. These tools help you plan your loan effectively. Online forums allow you to connect with others. Users share their experiences and advice on these platforms. E-books and articles cover various aspects of collateral loans. They explain complex terms in simple language. Taking advantage of these resources can be beneficial.

Why Use Property as Collateral?

-

Lower Interest Rates: Secured loans are generally cheaper. We’re talking about rates ranging from 6.5% to 11% compared to the hefty 15% to 30% of unsecured loans. Why? Because collateral makes lenders feel safer.

-

Bigger Loans: You can get up to 90% of your property’s equity. Imagine that being anywhere from $50,000 to $1 million, depending on your property’s worth.

-

Flexible Use: The funds you get can be spent on a variety of things. Need to expand your business? Consolidate debt? Or maybe pay for personal expenses?

-

Tax Perks: If you’re using a home equity loan or HELOC for home improvements, you might get some tax deductions. But remember, the IRS has limits, like $750,000 in debt.

Things to Watch Out For Using Property as Collateral

-

Foreclosure Risk: Miss your payments? You might lose your property. In some places like California, it could happen pretty fast—3 to 6 months.

-

Reduced Equity: Borrowing against your home means you own less of it. This could make selling or refinancing tricky later.

-

High Costs: Those closing costs and fees can add up quickly. We’re talking 2% to 5% of the loan. Plus, don’t forget the ongoing interest.

-

Market Fluctuations: If your property’s value drops, you could owe more than it’s worth. That’s a tough spot to be in.

-

Legal Concerns: Be honest about your financials and property details. Mistakes here can lead to penalties or even loan denial.

Tips for Borrowers

-

Shop Around: Look at different lenders. Compare their APRs, fees, and terms. Websites like Bankrate or NerdWallet can help.

-

Boost Your Credit Score: Pay off debts and avoid new credit inquiries before applying. It can help you get better rates.

-

Get a Professional Appraisal: Make sure you know your property’s true value. This helps you get the most out of your loan.

-

Consult an Attorney: Especially for commercial properties, have a lawyer check your loan agreements. You want to avoid tricky terms like prepayment penalties.

-

Understand Foreclosure Laws: Different states have different rules. Knowing yours can help protect your rights.

-

Keep a Financial Cushion: Have savings to cover payments if your income takes a hit. Avoiding default is key.

-

Explore Alternatives: If using your property feels too risky, think about unsecured loans, personal savings, or SBA loans.

Remember, using property as collateral can be a powerful tool, but it’s not without its risks. Make sure you’re informed and prepared to make the best decision for your situation.

Frequently Asked Questions

How Do I Use Property As Loan Collateral?

Using property as collateral involves pledging real estate to secure a loan. The lender assesses the property’s value and condition. If approved, the property guarantees loan repayment. Failure to repay may result in the lender taking possession of the property.

What Types Of Loans Accept Property Collateral?

Property collateral is accepted for mortgages, home equity loans, and secured business loans. These loans typically offer favorable terms due to reduced lender risk. Approval depends on the property’s value, your credit score, and income stability.

Are There Risks In Using Property As Collateral?

Yes, using property as collateral carries risks. If you default, the lender may seize your property, affecting your financial stability. It’s crucial to assess your ability to repay and understand the loan terms before proceeding.

How Is Property Value Assessed For Collateral?

Property value is assessed through professional appraisals. Appraisers consider factors like location, condition, and market trends. Accurate assessments ensure the loan amount reflects the property’s true value, protecting both borrower and lender.

Conclusion

Securing a loan with property as collateral can be smart. It offers lower interest rates and larger loan amounts. Ensure your property value meets the lender’s requirements. Prepare necessary documents like title deeds. Understand the risks involved, especially if you fail to repay.

Losing your property is a real possibility. It’s crucial to plan your finances wisely. Consult a financial advisor for personalized advice. They can help you make informed decisions. Remember, borrowing responsibly is key to protecting your assets. Make sure you choose the right lender for your needs.

Stay informed and confident in your choices.

Monica M. Watkins stands as a prominent authority in the realm of investment, recognized for her expertise as a “how-to” invest expert. With a robust background in finance and a keen understanding of market dynamics, Monica M. Watkins has become a trusted source for practical insights on investment strategies. Her career is characterized by a commitment to demystifying the complexities of financial markets and offering actionable guidance to both novice and seasoned investors. Whether unraveling the intricacies of stock market trends, providing tips on portfolio diversification, or offering guidance on risk management, Monica M. Watkins’s expertise spans a wide spectrum of investment-related topics. As a “how-to” invest expert, she empowers individuals with the knowledge and tools needed to navigate the ever-changing landscape of investments, translating complex financial concepts into accessible and actionable advice. Monica M. Watkins continues to be a guiding force for those seeking to make informed and strategic investment decisions, contributing significantly to the broader discourse on wealth-building and financial success.